Risk management/Operational risk

The tipping point

LOSS MANAGEMENT

SOX internal control costs decline

MANAGEMENT INTELLIGENCE

Sarbanes-Oxley: not winning any popularity contests

The US's Sarbanes-Oxley legislation is proving pretty unpopular within the industry as shown by our monthly OR&C Intelligence survey. Ellen Davis reports

Honesty and transparency 'are key'

MANAGEMENT INTELLIGENCE

Briefs

MANAGEMENT INTELLIGENCE

Flag-waving (not wavering)

As an American living in London, I've been acutely aware of the differences a small body of water can make to people's perceptions on certain issues.

The broadening scope of op risk management

Op risk programmes are no longer just about Basel II, according to the latest OR&C Intelligence survey. Ellen Davis reports

Corporate action spending to rise

MANAGEMENT INTELLIGENCE

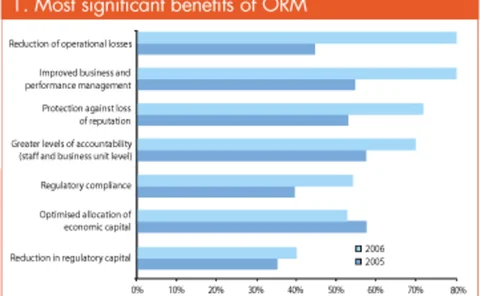

Operational risk continues measured progress

Expected benefits drive progress. By Protiviti's Michael Schuchardt and Brian Boyd

A captive audience

INSURANCE CAPTIVES

Briefs

MANAGEMENT INTELLIGENCE

Regulators eye equity derivatives

MANAGEMENT INTELLIGENCE

Isda survey finds error rates rising

MANAGEMENT INTELLIGENCE

MiFID documents release delayed as FSA waits on EU

MANAGEMENT INTELLIGENCE

New US NPR questions

The US notice of proposed rulemaking (NPR) has finally been published.

The fat tail

Minh-Tri Nguyen and Martin Ottmann aim to quantify op risk with multi-stage curve fitting and extreme value theory applied with the loss distribution approach

Briefs

MANAGEMENT INTELLIGENCE