Stress-testing

Comprehensive Capital Analysis and Review stress tests: is regression the only tool for loss projection?

The authors of this paper present a cross-sectional stress test analysis of major US banks.

CCP stress tests could help buy side pick winners

BlackRock exec calls for standardised test before European clearing starts

SEC’s Piwowar doubts CCPs should clear some instruments

Concern that historical price series volatility will not reflect jump-to-default risk

Riskology: What money markets can teach hedge funds

SEC stress tests provide foresight of damaging scenarios and increase time to react

Stress testing and modeling of rating migration under the Vasicek model framework: empirical approaches and technical implementation

This paper is concerned with stress testing the Vasicek model by extending the correlation structure for nondefault ratings. Two models are proposed.

Flawed reliance on VAR a systemic risk for insurers

Solvency II has its weaknesses, says writer and consultant René Doff

A dynamic approach to intraday liquidity needs

This paper studies the intraday liquidity needs of systemically important entities using simulations of the various Colombian financial market infrastructures (FMIs). The paper shows that if liquidity in another FMI (based on the proprietary positions of…

Santander op risk head aims to "get off bottom rung" after CCAR fail

Bank fell short this year on qualitative op risk governance issues

Q&A: Iosco’s Medcraft on CCP stress testing

CPMI-Iosco launch fact-finding mission on CCP risk management

Cutting Edge introduction: Creative stress testing

New stress-testing method offers a break from decades-old traditio

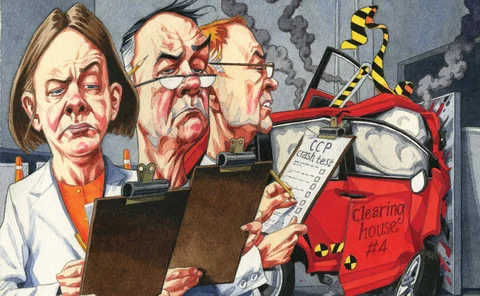

Who will be the dummy in CCP crash-tests?

Clearing houses, banks and regulators could all be caught in the wreckage

CCP stress-test rifts emerge as review gets underway

Banks, clearing houses and regulators all divided on question of standardised tests

Stress testing in non-normal markets via entropy pooling

Ardia and Meucci introduce a parametric entropy pooling approach to portfolios stress testing

EU risks have intensified, financial supervisors warn

Financial sector struggling with macro and operational risks

The hidden risks in dormant Basel III bond rule

Growing sovereign bond portfolios face new risks and mixed messages

SSM: banks fret over giant supervisor's first steps

New watchdog a great idea in theory, banks say - but early months have been difficult

ECB adviser admits more clarity needed over stress tests

Regulators criticised for reticence over why they rejected some test results

Fragile markets prompt banks to rethink tail risk

BNP Paribas and BTMU tout ‘scalable’ stress testing

What if operational risk asked more 'what if' questions?

Banks and regulators urged to up their game in stress tests and scenario analysis

LCH warns on CCP ‘auction risk’

CCP stress tests should consider possibility of failed auctions

Time to see models and shocks for what they are

Market shocks are earthquakes, not a game of roulette

UK stress tests to cover trading book illiquidity and FVA

Bank of England to apply price shocks based on unwind periods

Standard stress tests could create more risk, CCPs warn

Diverse products and risk profiles make standardised stress testing difficult