Default risk

Spanish banks allowed to ignore default risk for sovereign bonds

Banco de España is one of a number of European supervisors allowing its banks to ignore a Basel 2.5 requirement to model default risk on government bonds

Risk Annual Summit: Bank deleveraging 'might not be cyclical'

Aircraft, shipping and project finance all set to lose out as banks seek to constrain capital consumption, panellists warn

Variable selection in default risk models

Research Papers

US distressed debt funds look to euro crisis for opportunities

Stressful situations

Planning for bankruptcy of a major counterparty

Backup plan

HKEx moves to introduce margins for cash clearing members

HKEx plans to beef up its risk management following the bankruptcy of Lehman Brothers in September 2008 by introducing margin rules and seeking more funds from cash clearing members. The move would bring cash clearing more in line with existing…

Defaults by stealth are rare: Marty Fridson column

Defaults by stealth are rare

The limitations of using correlation in default prediction

Market analysis: Correlation and default

'An explosion of sovereign debt'

'An explosion of sovereign debt'

LBOs remain vulnerable to restructuring, says Pimco’s Jessop

The current low default rate in the high yield market does not tell the full story, the executive vice-president and portfolio manager at Pimco tells Credit.

China's bond laws remain a 'quagmire' for foreign investors, warns advisory firm

Investors in Chinese corporate bonds may struggle to recover their money in the event of a bankruptcy, according to FS Asia Advisory.

Execs would not be surpised if Eurozone shrinks, report claims

RBC Capital Markets survey say Greece most likely country to leave the eurozone.

Debt-ridden Spain and Portugal face new threats to credit status

Clouds are gathering over the Iberian peninsula. Attention is shifting from Greece, given temporary respite by the EU-IMF bailout, to Spain and Portugal as fears mount over their fiscal deficits and spiralling unemployment figures.

Market Analysis: Effective credit risk analysis

Market participants are conducting credit risk analysis on a growing number of counterparties, many of which are smaller, non-public and unrated firms, says S&P.

Greece faces legal problems in exiting Eurozone

If the €110 billion International Monetary Fund-Eurozone bailout fails and Greece is forced to dump the euro, legal experts say there would be no easy way out of its euro-denominated debts.

Looming junk bond glut threatens high yield returns

US high yield issuance has soared in the past year, but an imminent wall of refinancings is raising longer-term concerns.

RMBS defaults still a worry for structured finance investors

Despite talk of economic recovery, structured finance investors in the US and Europe remain concerned about defaults and losses on RMBS deals, according to S&P research.

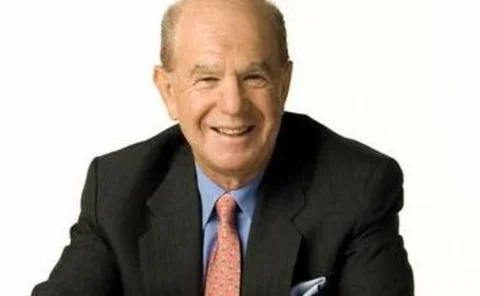

Z-Score architect launches new rating metrics: Edward Altman profile

Edward Altman, the high yield and credit risk expert, tells Credit that his new initiative for evaluating creditworthiness of non-financials has an error rate almost half that of the rating agencies.

Bilateral counterparty risk with application to CDSs

Previous research on credit valuation adjustments (CVAs) with correlation between underlying and counterparty default, including volatilities of both, assumed unilateral default risk. However, the crisis prompted counterparties to ask institutions to…