Swaps data: Sonia growth spreads down the curve

New figures show boom in sterling OIS swaps is not limited to short-dated trades

Last month’s article looked at some of the products that – if regulators have their way – will replace Libor-linked instruments before Libor itself can die. It was a popular piece, but the analysis was hampered by the absence of recent data on global cleared swap volumes by tenor. On its face, rapid growth in Sonia-referencing interest rate swaps looked encouraging – but to say how encouraging, you’d need to see liquidity propagating along the curve, rather than pooling exclusively in the shortest tenors.

As luck would have it, I have since managed to get my hands on such data – so, let’s go back and take a closer look.

Sonia swaps

In sterling, the Bank of England took over as the administrator of Sonia in April 2016. Two years later, it reformed the benchmark by including bilaterally negotiated transactions alongside brokered transactions, with a resulting three-fold increase in the underlying population, averaging £50 billion ($65.4 billion) daily.

At the same time, the working group on sterling risk-free reference rates selected Sonia as its preferred benchmark and has been working to catalyse a broad-based transition to Sonia. Let’s see what the data reveals about the progress so far.

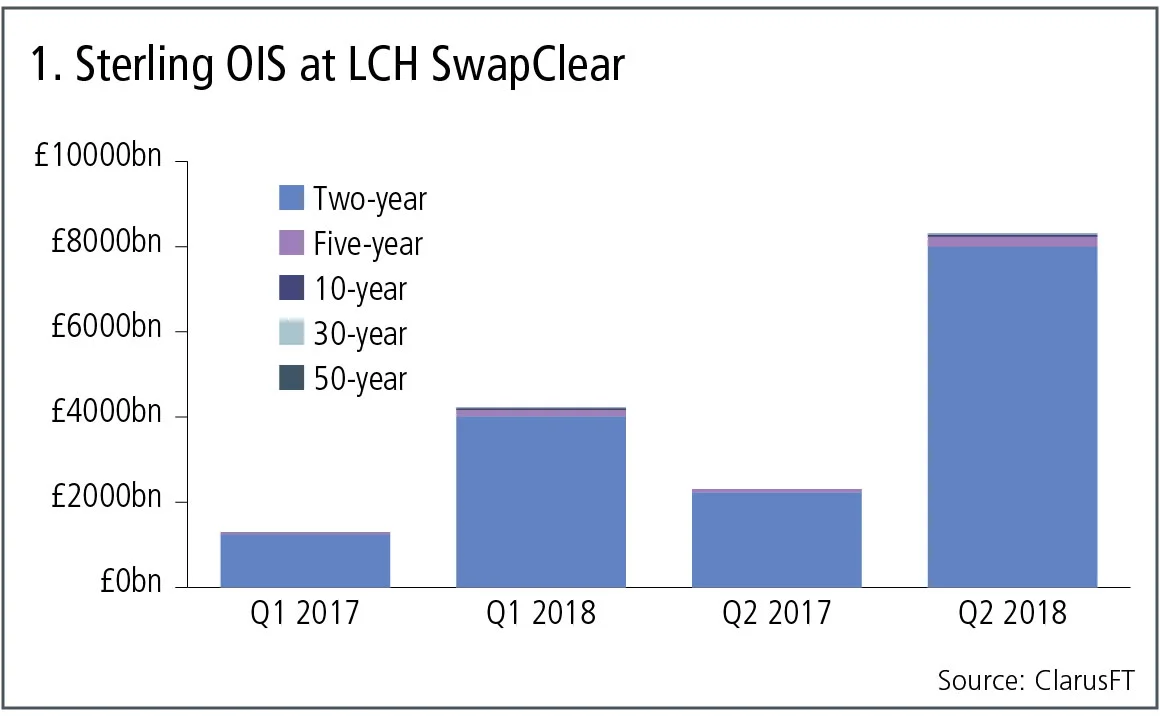

Figure 1 shows:

- Large increases, comparing quarters in 2018 with a year earlier.

- The first quarter of 2018 with £4.2 trillion gross notional, massively up from the first quarter of 2017.

- The second quarter of 2018 with £8.3 trillion gross notional, also much higher than the year-earlier quarter.

- Volumes massively dominated by tenors below two years, but larger slivers for tenors between two- and five-year and above starting to become visible in this year’s data.

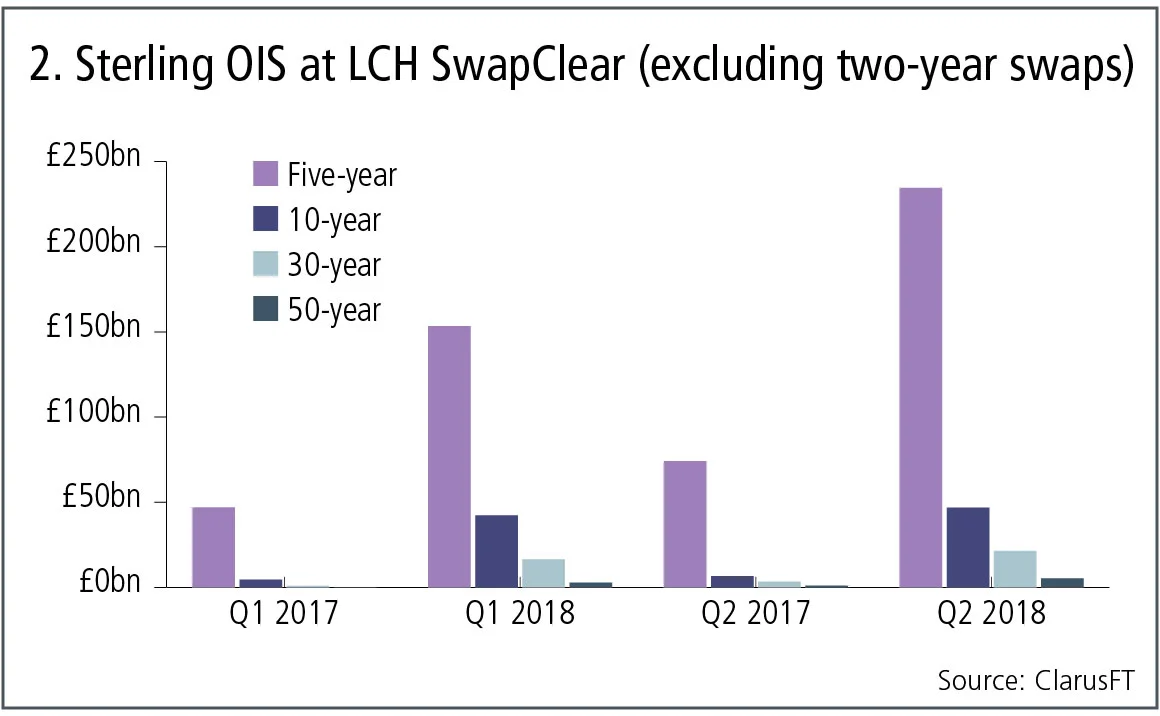

Let’s exclude the sub-two-year bucket and focus on volume in the longer tenors.

Figure 2 shows:

- The two- to five-year tenor showing strong growth and volumes reaching £235 billion in the second quarter of 2018.

- The five- to 10-year, 10- to 30-year and 30- to 50-year all showing much higher volumes year-on-year, with £47 billion, £22 billion and £5 billion respectively.

So, not huge volumes, but good increases and encouraging growth in longer-dated swap tenors. That looks like a good first step, but is it evidence of the transition regulators are looking for?

Sterling swaps

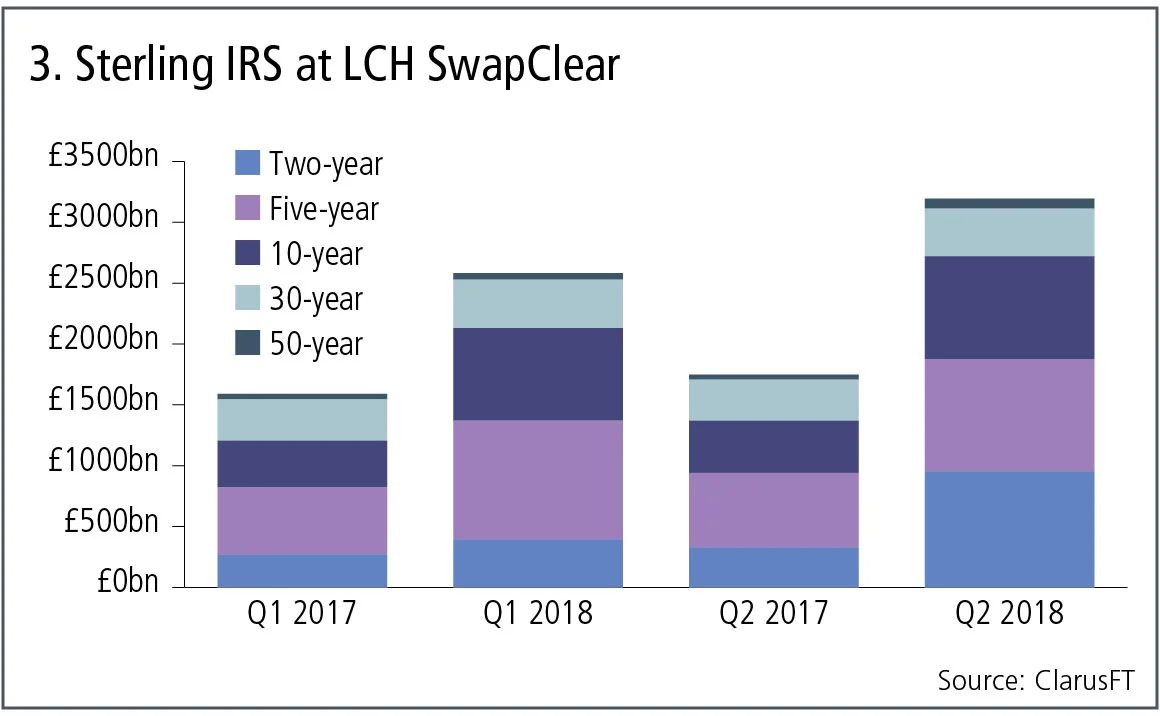

To answer that we need to look at the volume of sterling Libor swaps for the same quarters.

Figure 3 shows:

- Good increases, comparing quarters in 2018 with a year earlier.

- The first quarter of 2018 with £2.6 trillion gross notional, up 60% from the first quarter of 2017.

- The second quarter of 2018 with £3.2 trillion gross notional, up 80% from the second quarter of 2017.

- Much more even distribution – relative to Sonia swaps – of gross notional by tenor, with the two- to five-year tenor the largest, generally followed by the five- to 10-year tenor.

So, no categorical evidence of a transition from sterling Libor to Sonia swaps; for that we would need to see flat or falling Libor swap volumes. But the respective rates of growth are very different, with Sonia swaps racking up over 200% growth, compared with 70% for Libor. That augurs well for Sonia’s future, but the tenor distribution shows the challenge ahead – it’s a long way from posting comparably meaningful volumes in tenors above two years.

Europe

The situation in Europe is very different. Declining Eonia volumes since the European Central Bank launched its large-scale asset purchase programme have resulted in the ECB working group recently selecting Ester – a brand-new rate – as the replacement for Eonia. For Euribor, the jury is out while reform efforts are underway.

Let’s take a look at euro swap volumes for both indexes to size the task ahead.

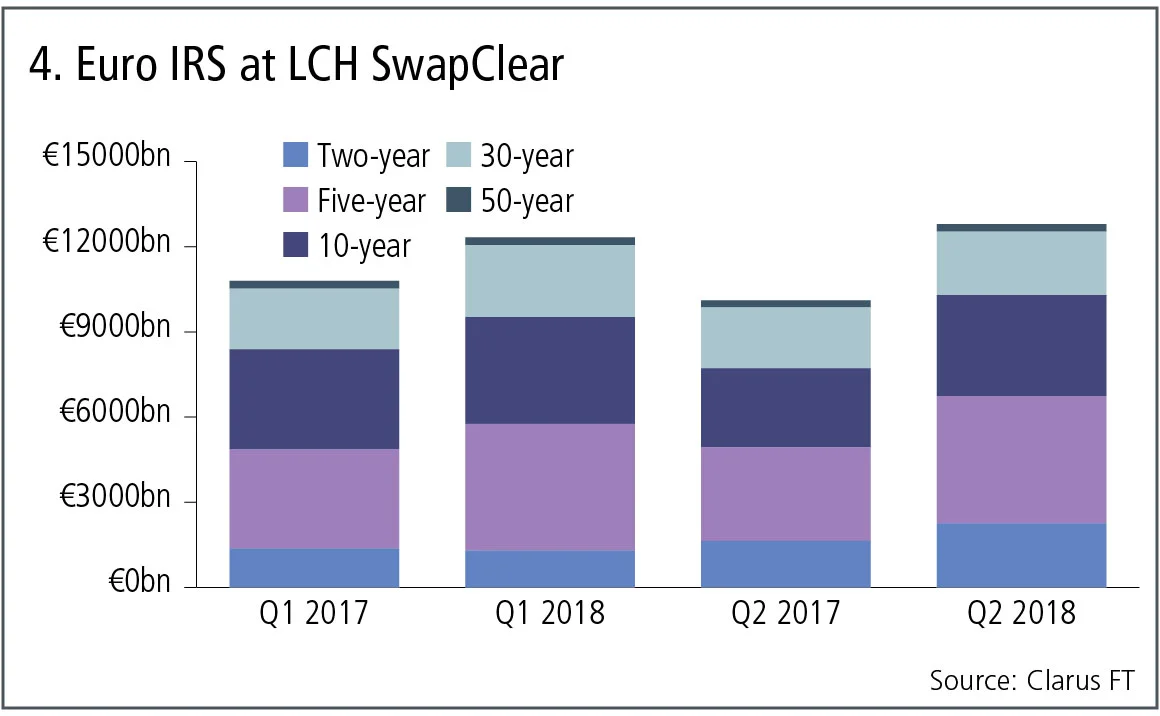

Figure 4 shows:

- Modest growth, comparing quarters in 2018 with a year earlier for Euribor swaps.

- The first quarter of 2018 with €12.3 trillion ($14.1 trillion) gross notional, up from €10.8 trillion in the first quarter of 2017.

- The second quarter of 2018 with €12.8 trillion gross notional, up from €10.1 trillion in the second quarter of 2017.

- The two- to five-year tenor is the largest, followed by the five- to 10-year tenor, with both the sub-two-year and 10- to 30-year tenor also showing massive volume.

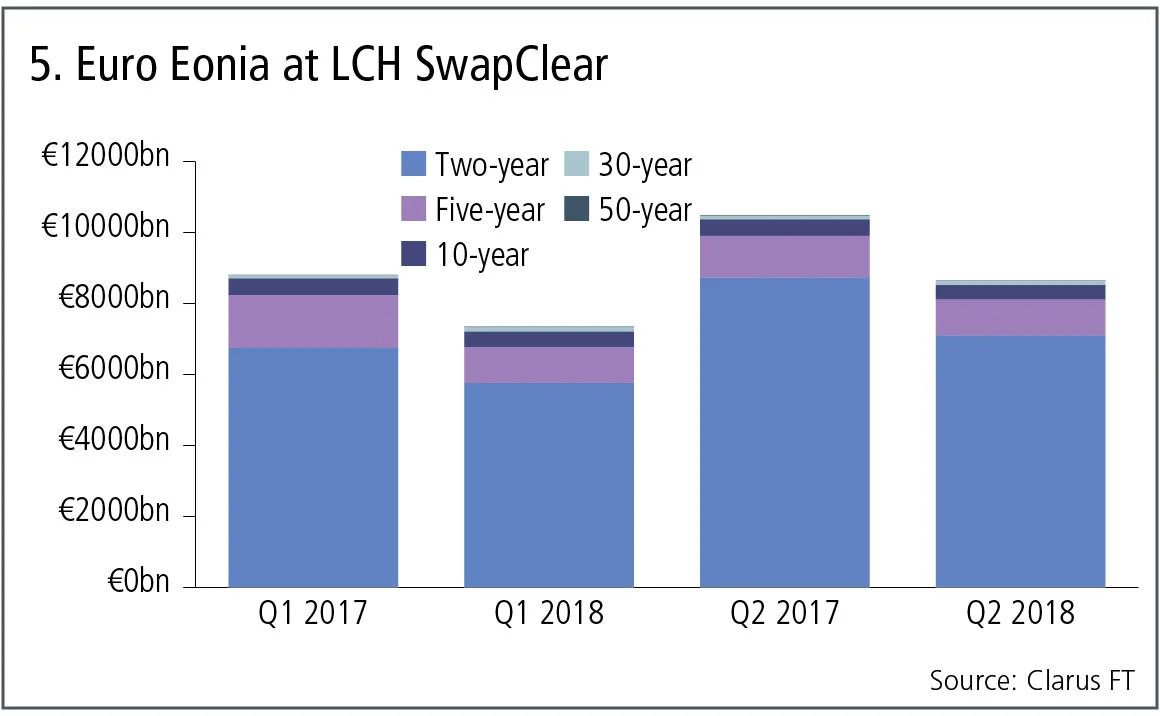

Figure 5 shows:

- Declines in Eonia volumes from a year earlier.

- The first quarter of 2018 with €7.3 trillion gross notional, down from €8.8 trillion in the first quarter of 2017.

- The second quarter of 2018 with €8.6 trillion gross notional, down from €10.5 trillion in the second quarter of 2017.

- While the sub-two-year tenor volumes dominate, there is substantial volume in the two- to five-year tenor and reasonable volume in the five-to 10-year tenor too.

Given the massive size of these volumes and the fact the ECB will only commit to publishing Ester by October 2019 – currently only a 10-day lagging pre-Ester is published – there is a lot of work to do. I’m not sure if the connotation here is more carrot or stick, probably equal measures of both are in order.

Only users who have a paid subscription or are part of a corporate subscription are able to print or copy content.

To access these options, along with all other subscription benefits, please contact info@risk.net or view our subscription options here: http://subscriptions.risk.net/subscribe

You are currently unable to print this content. Please contact info@risk.net to find out more.

You are currently unable to copy this content. Please contact info@risk.net to find out more.

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. Printing this content is for the sole use of the Authorised User (named subscriber), as outlined in our terms and conditions - https://www.infopro-insight.com/terms-conditions/insight-subscriptions/

If you would like to purchase additional rights please email info@risk.net

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. Copying this content is for the sole use of the Authorised User (named subscriber), as outlined in our terms and conditions - https://www.infopro-insight.com/terms-conditions/insight-subscriptions/

If you would like to purchase additional rights please email info@risk.net

More on Comment

Falling T2 balances bode well for eurozone’s stability

Impact of fragmentation would be less severe today than in 2010s, says Marcello Minenna

Op risk data: Tech glitch gives customers unlimited funds

Also: Payback for slow Paycheck Protection payouts; SEC hits out at AI washing. Data by ORX News

Op risk data: Lloyds lurches over £450m motor finance speed bump

Also: JPM trips up on trade surveillance; Reg Best Interest starts to bite. Data by ORX News

Georgios Skoufis on RFRs, convexity adjustments and Sabr

Bloomberg quant discusses his new approach for calculating convexity adjustments for RFR swaps

In a world of uncleared margin rules, Isda Simm adapts and evolves

A look back at progress and challenges one year on from UMR and Phase 6 implementation

Op risk data: Morgan Stanley clocked in block trading shock

Also: HSBC deposit guarantee gaffe; Caixa hack cracked; reg fine insult to cyber crime injury. Data by ORX News

Digging deeper into deep hedging

Dynamic techniques and GenAI simulated data can push the limits of deep hedging even further, as derivatives guru John Hull and colleagues explain

How AI can give banks an edge in bond trading

Machine learning expert Terry Benzschawel explains that bots are available to help dealers manage inventory and model markets

Most read

- Industry urges focus on initial margin instead of intraday VM

- For a growing number of banks, synthetics are the real deal

- Did Fed’s stress capital buffer blunt CCAR?