This article was paid for by a contributing third party.More Information.

Options to mitigate the challenges of index cessation fallbacks and conversion

This has so far been a defining year for index cessation, Isda’s fallbacks protocol and central counterparty conversions. TriOptima insists that now is the time for firms to get their interest rate swap portfolios in order before year-end

We came to learn a great deal about benchmark reform over the first few months of 2021. In what was always going to be a defining year, there is now greater clarity over index cessation, the derivatives fallbacks, as well as the conversion mechanisms being proposed by central counterparties (CCPs) for the impacted trades they clear.

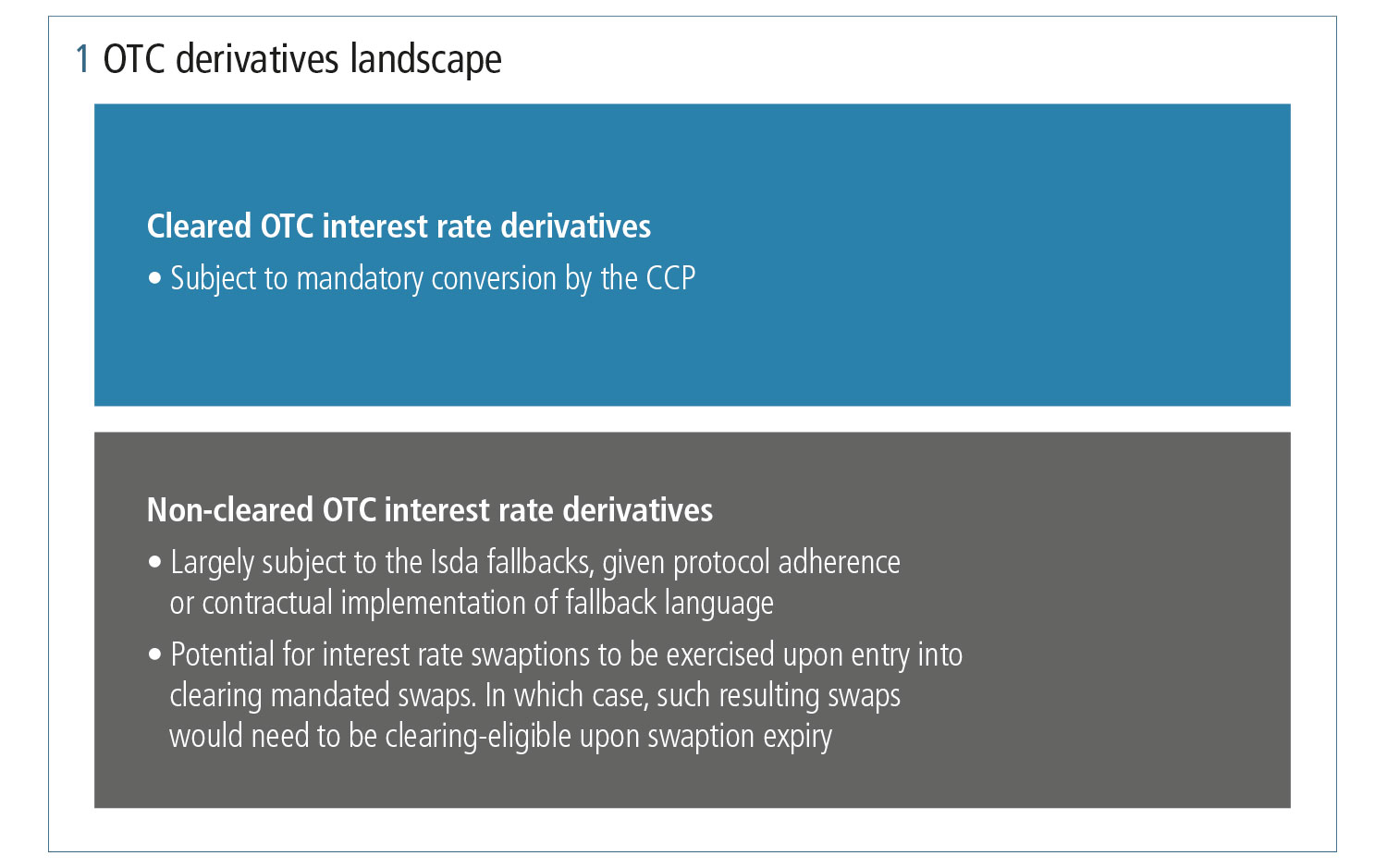

All in all, we can consider the impact of index cessation across the landscape for over-the-counter (OTC) derivatives as presented in figure 1.

Known index cessation timeline

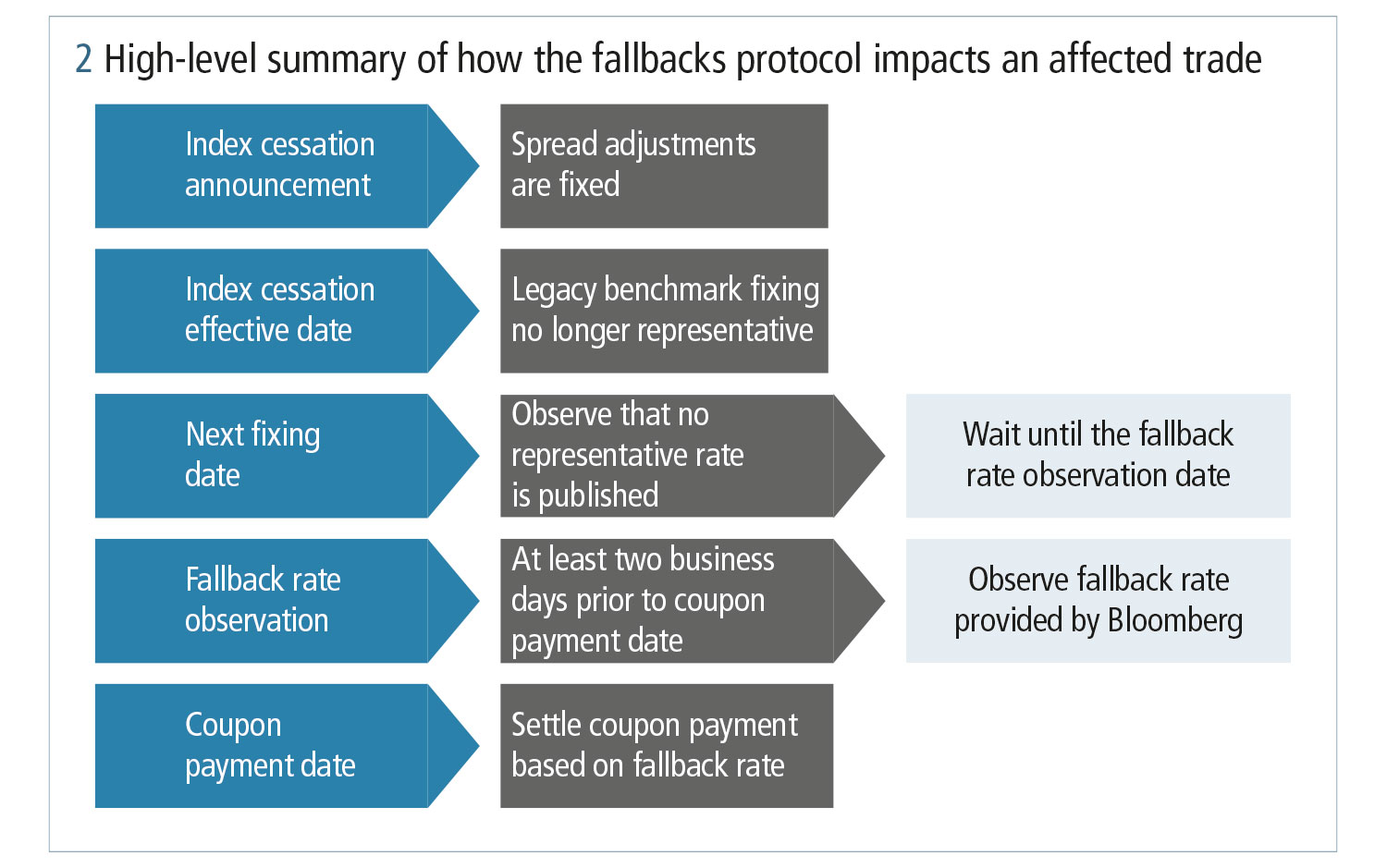

Since March 5, 2021, the spread between the legacy ICE Libor fixing and the compounded-in-arrears alternative risk-free rate (RFR) has been determined under the process defined by the International Swaps and Derivatives Association (Isda) 2020 Ibor fallbacks protocol. This spread represents the rate that will be added to a compounded in-arrears calculation of the alternative RFR in order to act as the fallback rate for an ICE Libor fixing that is either deemed no longer representative or is not published on a given fixing observation date.

With the fallback spread adjustments now being fixed and published, it removes one source of uncertainty around the cessation. The triggering of the fallbacks has provided market participants with greater legal certainty in relation to outstanding ICE Libor transactions. The industry’s focus can now shift to implementing the fallbacks protocol for legacy transactions executed on the ICE Libor benchmarks, as well as the associated supplemental fallback language for new swap transactions on the benchmarks.

Fallback implementation challenges

It is now apparent the complexities of maintaining a portfolio of trades on legacy benchmarks and building processes around the fallbacks present numerous challenges to market participants:

- Measuring the impact of the fallbacks. Perhaps one of the first actions for a firm is to estimate the impact of the fallbacks and the spread adjustment on their portfolio. Some may consider any post-cessation legacy benchmark exposure to be alternative benchmark exposure due to the fallback language. This will likely depend on acceptance of the doctrine that the market has already priced cessation into observable legacy benchmark swap rates, and is something firms will need to determine for themselves.

- Judging the all-in cost of supporting the fallback process until maturity. This includes the implementation cost of systems upgrades, revised operational processes, internal training and the opportunity cost of not proactively converting from legacy benchmarks or potentially utilising key resources towards other revenue-generating projects. In a year when firms are not only dealing with benchmark reform, but also the next phase of uncleared margin rules and adoption of new capital rules in the standardised approach for counterparty credit risk, supporting each of these changes will inevitably come at a cost.

- Understanding the firm’s ability to hedge and manage post-trade events in the legacy benchmark portfolio. It is too early to know how the market’s appetite for new trades in legacy benchmarks will be impacted, even if such trades are purely to offset existing risks. A typical dealer swap portfolio contains transactions with non-standard market conventions and illiquid trades with embedded optionality, as well as trades that are direct hedges to cash transactions that have been maintained over years. Common among all these product types is the need to maintain active cashflow reconciliation once the fallbacks are implemented. In a forward-looking benchmark world, the next coupon payment is known well in advance of its scheduled payment. Falling back to a compounded-in-arrears rate, on the other hand, leaves a very short amount of time to identify booking discrepancies that could lead to payment disputes. TriOptima’s triResolve service for portfolio reconciliation of OTC derivatives transactions is uniquely positioned to assist market participants, given the limited amount of time available to both detect and resolve potential payment disputes.

This is where a firm must consider all of its options. Already mentioned is how the fallbacks protocol and the associated supplement have provided legal certainty over the continued performance on contracts featuring legacy benchmarks. Firms are now able to consider how they can achieve an outcome that is economically equivalent to the fallbacks, but without having to maintain potentially cumbersome fallback processes. Fallback language can be viewed as a necessary safety net, but it shouldn’t provide motivation to run legacy benchmark exposure through to a trade’s maturity. This may place a burden on booking and risk systems, as well as potentially the cost of hedging activities.

Reducing legacy benchmark transactions

By using triReduce’s benchmark conversion mechanism, firms can proactively and iteratively reduce their legacy benchmark exposures and convert them to their chosen alternative benchmarks. Market participants can establish control over the conversion:

- Risk-based tolerances can be used to control impacts using the same measures that a firm manages every day. In turn, firms benefit from enhanced control over the pace of their compression and conversion from legacy benchmarks.

- Participants submit their own mid-market valuations for all trades in their portfolio, enabling cost-effective compression and conversion.

- Whether a portfolio-based or transaction-level approach is adopted, the resulting risk replacement swaps can take many forms:

- In the case of OTC interest rate swaps, the risk replacement trades can be truly market-standard trades or have the fallback spread adjustment applied to the floating leg. Eligible trades could also be cleared, which they will be if mandated.

- For cross-currency swaps, it is possible to convert just one leg at a time or convert both legs in a single step. LCH SwapAgent trades are eligible for compression and conversions, and SwapAgent is also a venue option to which the resulting risk replacement trades can be sent.

Collectively, these should provide tremendous assistance, affording participants the ability to take back some control over benchmark reform. It also means that there is a method of conversion for all OTC swap market participants.

Opportunities beyond cleared portfolios

Much of any remaining non-cleared portfolio consists of trades that are simply not eligible for clearing. These are interest rate derivatives with optionality, swaps that are too illiquid for a CCP to consider as eligible, or cross-currency swaps, which – for the most part – are not clearing-eligible. Adding to that a portion of swaps that are clearing-eligible would in theory generate additional cost and/or risk imbalances that make the act undesirable. For such trades, it is likely that tailored solutions will be necessary for bilateral counterparts or groups of counterparties to be able to agree on a method for exposure reduction or conversion.

There are portfolio-based and trade-level conversion options available for non-cleared trades. At a portfolio level, the objective would be to compress as much legacy benchmark exposure as possible, while simultaneously converting interest rate exposure to alternative benchmarks to achieve greater degrees of legacy benchmark exposure reduction, such as the process for cleared trades. The key difference here is that the choice of replacement trade can be influenced by the participants in the exercise. For instance, it may be preferable to introduce additional cleared risk-compensating swaps to minimise the residual cash that might be generated. Likewise, participants may consider introducing a spread onto the floating leg benchmark to account for differences between the legacy and the chosen replacement benchmarks.

Adding a spread also underlies how a trade-level conversion might be performed because firms that are likely to prefer this method are also likely to favour cashflow preservation. Performing the conversion at a trade level calls for amending as few parameters of a transaction as possible, relating mostly to the legacy benchmark floating leg(s). Firms will be looking at how the cashflow profile might be impacted by the conversion through the introduction of payment lags, as well as the preservation of representative legacy benchmark fixings.

It would seem we are heading towards an unprecedented end to the year as the market readies itself for index cessation and the associated CCP conversion and Isda fallback implementation. Compression and conversion are themes that will likely surround these milestones and, make no mistake, now is the time for firms to act and take control of their OTC interest rate swap portfolios.

Further information

Contact info@trioptima.com to discuss your benchmark conversion needs or to learn more about triReduce’s Benchmark Conversion functionality

Libor Risk – Quarterly report Q2 2021

Read more

All information contained herein (“information”) is for informational purposes only, is confidential and is the intellectual property of CME Group Inc. and/or one of its group companies (CME). The Information is directed to equivalent counterparties and professional clients only and is not intended for non-professional clients (as defined in the Swedish Securities Market Law (lag (2007:528) om värdepappersmarknaden)) or equivalent in a relevant jurisdiction. This information is not, and should not be construed as, an offer or solicitation to sell or buy any product, investment, security or any other financial instrument or to participate in any particular trading strategy. CME and the CME logo are trademarks of CME Group. TriOptima AB is regulated by the Swedish Financial Supervisory Authority for the reception and transmission of orders in relation to one or more financial instruments. TriOptima AB is registered with the US National Futures Association as an introducing broker. For further regulatory information, please see www.cmegroup.com. TriOptima holds a permit under Section 49A of the Israeli Securities Law, however, TriOptima’s operations are not subject to the supervision of the Israel Securities Authority. This permit does not constitute an opinion regarding the quality of the services rendered by the permit holder or the risks that such services entail. TriOptima’s services are designed exclusively for qualified investors in accordance with Israeli law. For further regulatory information, please see www.cmegroup.com

TriOptima AB. Registered Address: Mäster Samuelsgatan 17, 111 44 Stockholm, Sweden.

Org no.: 556584-9758.Copyright © 2021 CME Group Inc. All rights reserved.

Sponsored content

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. Printing this content is for the sole use of the Authorised User (named subscriber), as outlined in our terms and conditions - https://www.infopro-insight.com/terms-conditions/insight-subscriptions/

If you would like to purchase additional rights please email info@risk.net

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. Copying this content is for the sole use of the Authorised User (named subscriber), as outlined in our terms and conditions - https://www.infopro-insight.com/terms-conditions/insight-subscriptions/

If you would like to purchase additional rights please email info@risk.net