Asia Risk - 2008-02-01

Articles in this issue

Structured stagnation

Editor's letter

Biting the bullet

Emerging-market loans

System overload

Private banks

Fluctuating tides

Freight derivatives

Asian payoff

Cover story

Supervising sharia

Special Report - Malaysia: Q&A

Clarification

News

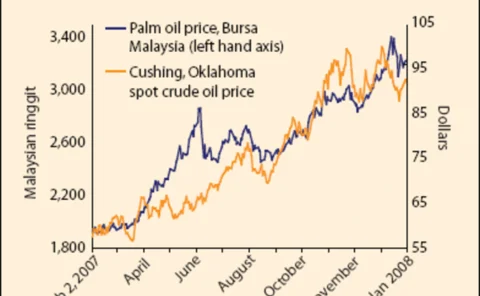

A volatile blend

Special Report - Malaysia: Palm oil

Collision course

Special Report - Malaysia: Regulation

The road ahead

Conference report

CDS confirmation backlog

Trade processing

Gaining momentum

Special Report - Malaysia

VAR: risk mitigant or amplifier?

Value-at-risk

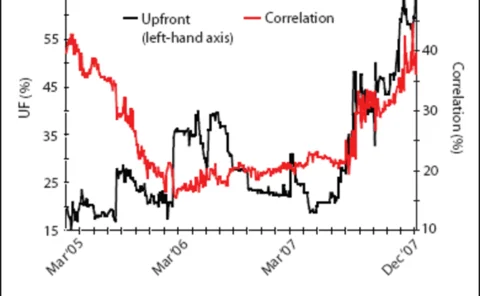

Factor models for credit correlation

Stewart Inglis and Alex Lipton describe dynamic and static factor models for credit correlation, and show how the static model can be calibrated to the market and used for the pricing of standard and bespoke tranches, including tranchelets

Growing Reliance

Profile

Airing a new scheme

Emissions trading

A new direction?

Structured products

iTraxx interest

Correlation trading

Hong Kong steps up Islamic finance ambitions

Government officials seek to leverage proximity to China

Correction

News

On the move

People