Asia Risk - 2007-05-01

Articles in this issue

What lies beneath

Editor's letter

Rate steepeners rise again

CMS spreads

Cfets' fx trading system launches

News in brief

Icap launches A$/NZ$ e-trading

News in brief

On the move

People

Emissions gain credit

Carbon finance

More CBO woes

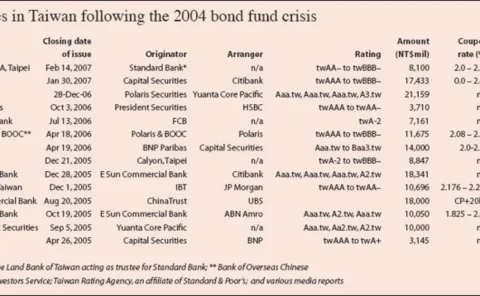

Taiwan

Spectron and GFI in Asian JV

News in brief

Markovian projection for volatility calibration

Vladimir Piterbarg looks at the Markovian projection method, a way of obtaining closed-form approximations of European-style option prices on various underlyings that, in principle, is applicable to any (diffusive) model. The aim is to distil the essence…

TT links to SGX

News

The power law

Masterclass

Singapore stumbles

Exchanges

HDFC Bank chooses Misys for rates

News in brief

Stuck on the margins

Prime broking

Supervisory clampdown

Korea regulation

Stunned by subprime

CDOs of ABSs

Set for meltdown?

Cover story